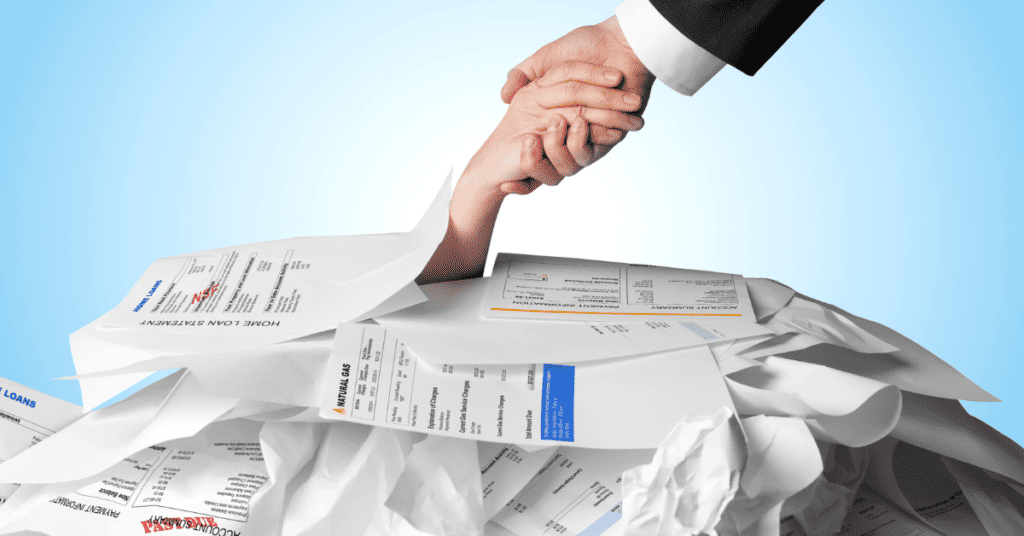

What is Debt Consolidation

Taking out a new debt relief program to pay off your existing debts is known as debt consolidation. In essence, you’re combining all of your loan payments into one. If you have several high-interest loans or credit cards, this can be an excellent alternative because you might be able to receive a debt consolidation loan with a lower interest rate.

In Canada, there are primarily two kinds of debt consolidation loans: secured and unsecured. Unlike unsecured loans, secured loans need collateral like a house or car.

A lump sum of money that you can use to pay down your current debts is often given to you when you take out a debt consolidation loan, especially for secured loans. After that, you will make one payment each month on your new loan,

➧ Benefits of Debt Consolidation

Consolidating debt has a number of advantages, including:

If you consolidate your debt, you’ll just have one monthly payment to make, which may be simpler to handle than making several payments to several creditors.

Fixed or low-interest rates:

For secured debt consolidation loans, If you have high-interest credit cards or loans, you might be able to acquire a debt consolidation loan at a better interest rate because it will be fixed and will not vary from one debt to another, which can help you save money over time. For unsecured Debt Relief Program Services in Canada, you can avail of lower interest rates as well.

Making timely payments on your debt consolidation loan might increase your credit score over time.

No risk of collateral loss:

If you choose an unsecured debt consolidation loan, you won’t need to be concerned about losing your house or car if you can’t make your payments.

What is Debt Settlement?

Debt settlement, commonly referred to as debt negotiation or debt relief, is the process of negotiating with your creditors to settle your obligations for less than you are owed. In essence, you’re asking your creditors to accept a single payment that is less than the full amount of your debt in exchange for forgiving the remaining balance.

Working with a debt settlement company or lawyer who will speak with your creditors on your behalf is normal for debt settlement. You’ll normally pay the debt settlement business on a monthly basis, and they’ll keep your money in an account until you have enough to reach a settlement.

Once a settlement has been achieved, you’ll pay your creditor a one-time sum and your debt will be regarded as fully settled. The fact that creditors could mark resolved debts on your credit record as “settled for less than the full amount” might have a detrimental effect on your credit score.

➧ Benefits of Debt Settlement

The following are a few advantages of debt settlement:

By negotiating with your creditors to take a lump sum payment that is less than the total of your debt, debt settlement can help you lower the total amount of debt you owe.

Because you’ll be making one large payment to pay off all of your obligations, you may be able to work out a deal with your creditors for lower monthly payments.

Debt settlement may be a quicker choice than other debt relief strategies because you might be able to pay off your debts in as little as 2-4 years.

Because debt settlement does not demand collateral, you will not lose your home or automobile if you default on the loan.

Which is Right for You: Debt Settlement or Debt Consolidation?

You may be unsure of which debt relief option is best for you now that you know more about debt consolidation and debt settlement. Depending on your unique financial situation and goals, the answer will vary.

Debt consolidation might be a suitable choice for you if you have a lot of high-interest debt and find it difficult to meet your monthly payments. You might be able to save money over time and reduce your monthly payments by combining your loans into one payment with a reduced interest rate.

On the other hand, debt settlement might be a better choice if you’re having trouble making your monthly payments and don’t have the income to sustain a debt consolidation program. Even if you don’t have the means to afford a traditional debt consolidation loan, debt settlement can help you lower the overall amount of debt you owe and make your monthly payments easier to manage.

However, it’s crucial to keep in mind that both will lower your credit score.

Ultimately, talking to a financial counselor or debt relief specialist is the best way to figure out which choice is ideal for you. They can assist you in evaluating your financial status and choosing the best Debt Relief Program Service in Canada.

“So take action now and ask National Debt Relief for assistance if you want to get out of debt and reclaim your financial freedom!”